I know a tax payer, a nonprofit organisation, that discovered that a ‘corporate tax collector’ that had been illegally collecting withholding tax from it, had never submitted the taxes withheld to Uganda Revenue Authority (URA)

When caught, officers of the cheating ‘corporate tax collector’ gave ridiculous excuses that they did not credit the tax payer because they did not have the tax identification number (TIN) of the tax payer. Liars!

The cheating ‘corporate tax collector’ engaged in foolery – generating phony tax credit certificates, which it gave to tax payers as evidence that it had delivered the taxes to URA, when in reality it had not.

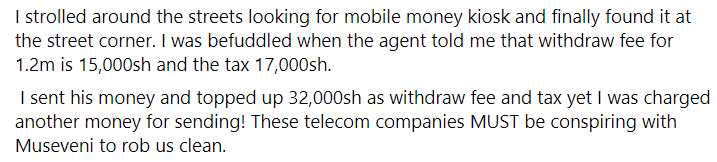

Mobile money tax example one:

Take mobile money tax for example, sincerely, those ‘corporate tax collectors’ have a lot of our money that is goes through them; money, which we often pay with pain to them for onward submission to URA.

Kakwenza Rukirabashaija on his Facebook wall

Kakwenza Rukirabashaija on his Facebook wall

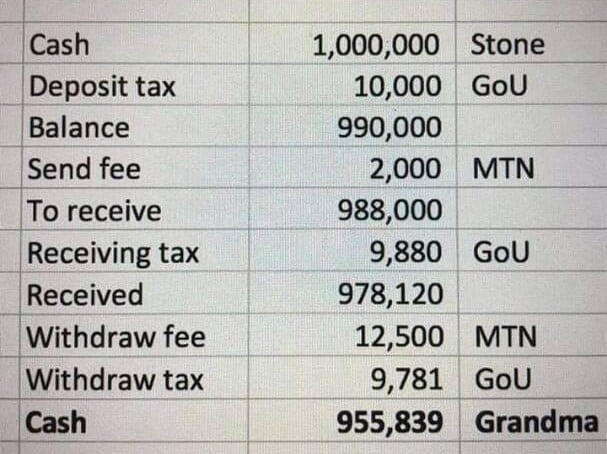

Mobile money tax example two:

Source: Joan Mugenzi’s Facebook wall

Source: Joan Mugenzi’s Facebook wall

Imagine the possibilities if all those ‘corporate tax collectors’ were submitting our taxes to URA in a timely and transparent manner. ‘Corporate tax collectors’ is where the focus of URA needs to be – doing audits of all those who claim the status ‘corporate tax collector’. And when caught cheating, they should be penalised heavily.

Let’s Chat…